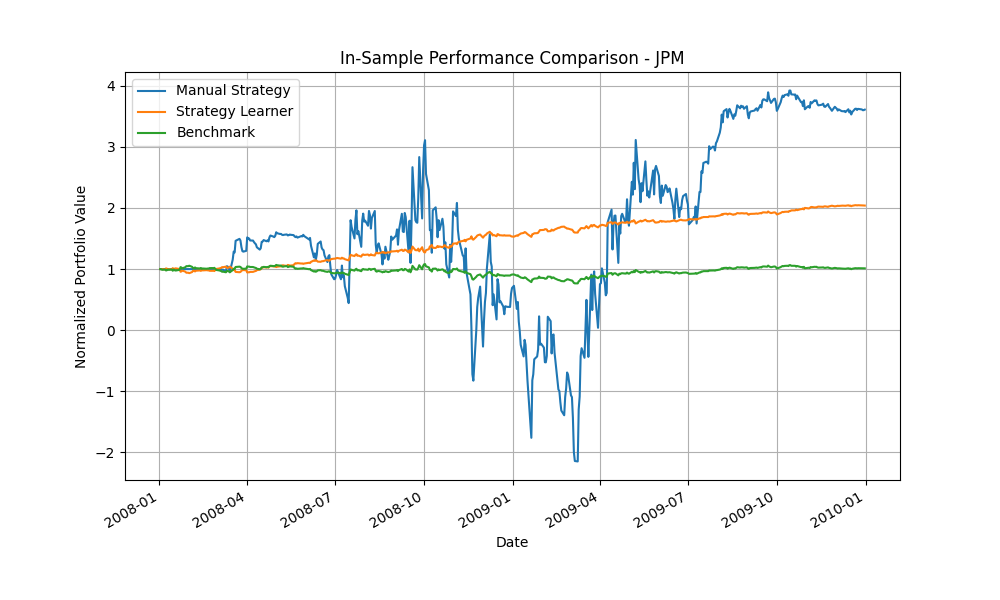

Performance Comparison

In this project, I examined two distinct trading strategies and compared them with a benchmark strategy. The first, a manual strategy, utilized well-established financial indicators like SMA, Momentum, and RSI to dictate trading decisions. It followed a rule-based approach, entering long or short positions based on specific criteria set by these indicators. The second, a Strategy Learner, adopted a machine learning approach through a custom-built RTLearner. This learner was designed to autonomously develop trading rules from historical data, aiming to adapt to market changes more fluidly than the manual method. The benchmark, representing a traditional buy-and-hold strategy, served as a reference to gauge the effectiveness of these two approaches.

Evaluating the performance of these strategies under varying market conditions revealed distinct differences. The manual strategy showed effectiveness in certain scenarios but struggled in highly volatile or stagnant markets due to its reliance on fixed rules. In contrast, the Strategy Learner, leveraging its learning capabilities, demonstrated a potential advantage in adapting to market volatilities. Its performance, compared to the consistent results of the benchmark strategy, highlighted the risks and potential rewards of active trading strategies. Notably, the Strategy Learner’s conservative trading approach, as opposed to the more aggressive manual strategy, indicated a calculated response to market trends.

A key component of this exploration was the RTLearner within the Strategy Learner. Its role in processing market data highlighted a stark contrast to the manual strategy’s fixed rules. The learner’s specific parameters, like leaf size and impact values, were crucial in its market navigation. A more detailed analysis of the RTLearner, including its parameter tuning and influence on trading outcomes, will be discussed later in the report. This will provide insight into the integration of machine learning in financial trading strategies.

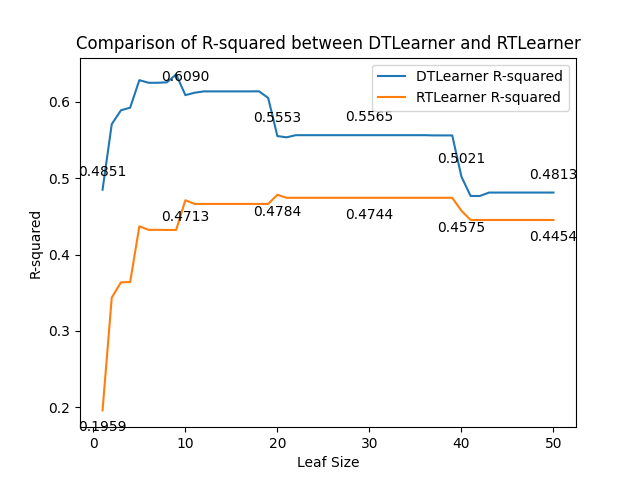

The RTLearner I used in this project is built in my earlier project "Assess Learners", in which I focused on comparing the Random Tree Learner (RTLearner) with the Decision Tree Learner (DTLearner) within the context of Classification and Regression Trees (CART). The key distinction of the RTLearner lies in its approach to feature selection; it randomly selects a feature to split on, as opposed to the DTLearner, which chooses based on feature correlation with the target variable. This random selection approach in RTLearner is designed to mitigate the risk of overfitting, a prevalent challenge in machine learning, by potentially capturing a broader range of patterns from the training data. However, this method also introduces the risk of underfitting, highlighting a crucial trade-off in model generalization.

The RTLearner's incorporation into the Strategy Learner was a critical element in my examination of trading strategies. It presented a novel method to autonomously develop trading rules from historical data, aiming to adapt more fluidly to market changes than the rule-based manual strategy. This adaptive capability of the RTLearner, supported by my hands-on experience and development using Numpy, was key to hypothesizing the performance variations between the learners. The randomized feature selection process, while mitigating overfitting, posed unique challenges in justifying feature selection decisions compared to the more predictable DTLearner.

The effectiveness of the RTLearner within the Strategy Learner, particularly against manual strategies and benchmark approaches, marked a significant aspect of my project. The experiments conducted aimed to determine if the RTLearner's method could balance essential market pattern recognition with the prevention of overfitting. The RTLearner's performance, especially in different market conditions, highlighted its potential in adapting to market volatilities and underscored the benefits and limitations of using randomized learning methods in financial trading strategies. This insight into the RTLearner's functionality within the Strategy Learner offers a comprehensive view of its role in modern financial trading systems.